Revenue Sharing Conflicts

Most retirement plans offer mutual funds in their retirement plan menu. How do mutual fund companies assess fees? If you participate in a retirement plan, have you received an invoice from the company asking for their fee, of course not. Mutual fund companies assess fees as a percentage of money invested in their funds. This percentage is known as the expense ratio.

Mutual funds are a collection of stocks, bonds or both. The unit value or Net Asset Value (NAV) that you see on your statement fluctuates daily based on the underlying value of stocks, bonds or both. The fund company will scrape a portion of the unit value (NAV) from the fund. The percentage they take off the top is based on the fund’s expense ratio and is expressed as a percentage of assets. In conclusion, the fee taken reduces the fund’s return.

For example, if the fund had a 1% expense ratio with an annual return of 6%, the actual return was 7% and the fund company reported a 6% annual return. Likewise, if the fund reported a -8% annual return, the fund actually had a -7% annual return and added the 1% fee to the return, resulting in a -8% annual return. From this example, with all else being equal, lower fees and expenses result in more favorable returns.

What is Revenue Sharing and how does it affect your account?

It is common for a mutual fund to offer several classes of shares, with the same investments but with different fees and expenses. What is a share class?

Some mutual fund companies will offer investors different types of shares, known as “classes.” Each class will invest in the same portfolio of securities (stocks and/or bonds) and have the same investment objectives and policies, but each class will have different shareholder services and/or distribution arrangements with different fees and expenses and, therefore, different performance results.

Why do mutual funds offer several different share classes?

Some fund companies will offer different share classes and set the fund’s expense ratio at different levels to pay for non-investment related services (fees are paid from the mutual fund company and paid to the retirement plan company / record keeper).

The types of services delivered by retirement plan companies include keeping record of participant accounts, statements, on-line services, trading, compliance testing and IRS filings (See Elements of a 401(k) for additional information). These payments from the mutual fund company for non-investment related services are often described as revenue sharing. These share classes with their range of costs, are intended to provide choices on how to pay for non-investment related services.

The diagram below provides an example of the impact on participants with equivalent balances:

A few of the problems that arise from revenue sharing are:

Identifying the level and recipient of revenue sharing

Conflicts associated with which investments are offered in the retirement plan

Disclosure – participants don’t know they are paying for these services

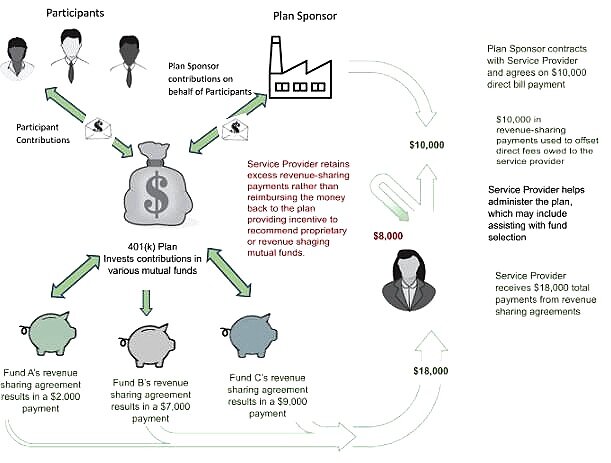

The issue for retirement plan sponsors is to make sure that they are selecting, and continuing to use, the appropriate—or prudent—share class. Why? Because the wrong share class can cost more money and, as a result, reduce retirement benefits—and, ultimately, lower standards of living in retirement. The diagram below demonstrates how revenue sharing arrangements can entail a conflict of interest for the service provider.